《山东大学学报(理学版)》 ›› 2023, Vol. 58 ›› Issue (11): 35-44.doi: 10.6040/j.issn.1671-9352.0.2022.096

王小刚( ),冯可馨*()

),冯可馨*()

Xiaogang WANG(),Kexin FENG*()

摘要:

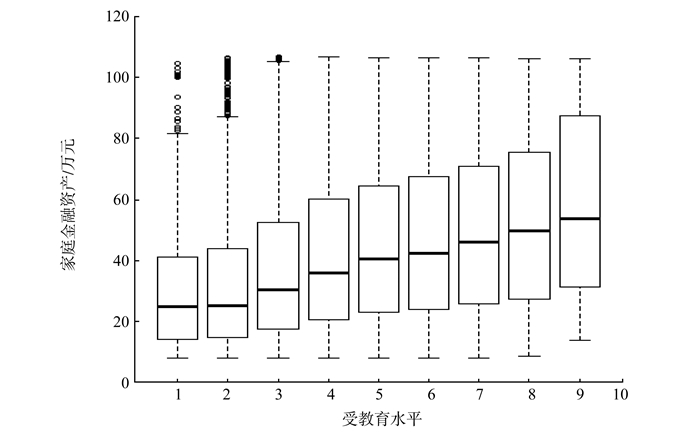

在删失分位数回归模型中引入分段线性结构, 改进原有模型仅考虑线性结构、静态性和无交互效应等缺陷。分段线性的前提假设使得部分协变量在不同状态下呈现不同结构且在变点处连续, 保留模型易于计算和解释性强的优点。基于格点搜索法得到变点位置和模型参数估计, 推导估计的大样本性质。数值模拟结果验证不同误差结构下变点和模型参数估计具有有效性和稳健性。实证分析表明家庭金融资产与受教育水平正相关, 且资产规模存在集聚效应, 资产规模越大的家庭其金融资产越多。受教育水平在本科之前存在一个变点, 突破受教育水平变点后, 不同规模家庭的金融资产都有质的提升, 但变点后高资产规模家庭的金融资产增速要高于中低资产规模家庭的增速。

中图分类号:

| 1 | 甘犁, 尹志超, 谭继军. 中国家庭金融调查报(2014)[M]. 成都: 西南财经大学出版社, 2015. |

| GAN Li , YIN Zhichao , TAN Jijun . China household finance survey report(2014)[M]. Chengdu: Southwestern University of Finance and Economics Press, 2015. | |

| 2 | 吴文生, 李硕, 谭常春, 等. 中国家庭风险资产配置的理论与实证: 基于信息不确定性视角下的研究[J]. 系统工程理论与实践, 2022, 42 (1): 60- 75. |

| WU Wensheng , LI Shuo , TAN Changchun , et al. The theory and evidence of Chinese household risk asset allocation from the perspective of information uncertainty[J]. Systems Engineering: Theory and Practice, 2022, 42 (1): 60- 75. | |

| 3 |

KOENKER R , BASSETT G . Regression quantiles[J]. Econometrica, 1978, 46 (1): 33- 50.

doi: 10.2307/1913643 |

| 4 |

POWELL J L . Censored regression quantiles[J]. Journal of Econometrics, 1986, 32 (1): 143- 155.

doi: 10.1016/0304-4076(86)90016-3 |

| 5 |

PORTNOY S . Censored regression quantiles[J]. Journal of the American Statistical Association, 2003, 98 (464): 1001- 1012.

doi: 10.1198/016214503000000954 |

| 6 | 刘生龙. 教育和经验对中国居民收入的影响: 基于分位数回归和审查分位数回归的实证研究[J]. 数量经济技术经济研究, 2008, 4, 75- 85. |

| LIU Shenglong . The impact of education and experience on residents' income in China: empirical research based on quantile regression and review quantile regression[J]. Journal Quantitative and Technical Economics, 2008, 4, 75- 85. | |

| 7 | FRUMENTO P , BOTTAI M . An estimating equation for censored and truncated quantile regression[J]. Computational Statistics & Data Analysis, 2017, 113, 53- 63. |

| 8 | 张倩倩, 郑茜, 王纯杰, 等. 删失分位数回归在医疗费用中的应用[J]. 数理统计与管理, 2018, 37 (6): 1050- 1062. |

| ZHANG Qianqian , ZHENG Xi , WANG Chunjie , et al. Application of censored quantile regression in medical cost[J]. Journal of Applied Statistics and Management, 2018, 37 (6): 1050- 1062. | |

| 9 | 李忠桂, 何书元. 右删失数据下分位数回归的光滑经验似然检验[J]. 应用概率统计, 2019, 35 (2): 153- 164. |

| LI Zhonggui , HE Shuyuan . Smoothed empirical likelihood testing for quantile regression models under right censorship[J]. Chinese Journal of Applied Probability and Statistics, 2019, 35 (2): 153- 164. | |

| 10 | KIM M , LEE S . Nonlinear expectile regression with application to Value-at-Risk and expected shortfall estimation[J]. Computational Statistics & Data Analysis, 2016, 94, 1- 19. |

| 11 | XIE Shangyu , ZHOU Yong , WAN A T K . A varying coefficient expectile model for estimating value at risk[J]. Journal of Business & Economic Statistics, 2014, 32 (4): 576- 592. |

| 12 | 刘晓倩, 周勇. 风险度量半参数变系数符合Expectile回归模型及应用[J]. 系统工程理论与实践, 2020, 40 (8): 2176- 2192. |

| LIU Xiaoqian , ZHOU Yong . The semiparametric varying-coefficient composite expectile regression model in risk measurement and its application[J]. Systems Engineering: Theory & Practice, 2020, 40 (8): 2176- 2192. | |

| 13 |

MUGGEO V M R . Estimating regression models with unknown break-points[J]. Statistics in Medicine, 2003, 22 (19): 3055- 3071.

doi: 10.1002/sim.1545 |

| 14 | HANSEN B E . Regression kink with an unknown threshold[J]. Journal of Business & Economic Statistics, 2017, 35 (2): 228- 240. |

| 15 |

ZHANG Feipeng , LI Qunhua . Robust bent line regression[J]. Journal of Statistical Planning and Inference, 2017, 185, 41- 55.

doi: 10.1016/j.jspi.2017.01.001 |

| 16 |

LI Chenxi , WEI Ying , CHAPPELL R , et al. Bent line quantile regression with application to an allometric study of land mammals' speed and mass[J]. Biometrics, 2011, 67 (1): 242- 249.

doi: 10.1111/j.1541-0420.2010.01436.x |

| 17 | ZHANG Feipeng , LI Qunhua . A continuous threshold expectile model[J]. Computational Statistics & Data Analysis, 2017, 116, 49- 66. |

| 18 |

ZHOU Xiaoying , ZHANG Feipeng . Bent line quantile regression via a smoothing technique[J]. Statistical Analysis and Data Mining: The ASA Data Science Journal, 2020, 13 (3): 216- 228.

doi: 10.1002/sam.11453 |

| 19 | SILVERMAN B W . Density estimation for statistics and data analysis[M]. London: Chapman & Hall, 1986. |

| 20 | 王小刚, 李冰. 含多个结构突变的分段线性Tobit回归模型及应用[J]. 统计与决策, 2021, 37 (19): 21- 25. |

| WANG Xiaogang , LI Bing . A piecewise linear Tobit regression model with multiple structural mutations and its application[J]. Statistics & Decision, 2021, 37 (19): 21- 25. | |

| 21 | 李实, 魏众, 古斯塔夫森B. 中国城镇居民的财产分配[J]. 经济研究, 2000, (3): 16- 23. |

| LI Shi , WEI Zhong , GUSTAFSSON B . Distribution of wealth among urban township households in China[J]. Economic Research Journal, 2000, 35 (3): 16- 23. | |

| 22 |

BROWN S , TAYLOR K . Household debt and financial assets: evidence from Germany, Great Britain and the USA[J]. Journal of the Royal Statistical Society (Series A: Statistics in Society), 2008, 171 (3): 615- 643.

doi: 10.1111/j.1467-985X.2007.00531.x |

| 23 | 牛树海, 杨梦瑶. 中国区域经济差距的变迁及政策调整建议[J]. 区域经济评论, 2020, 2, 37- 43. |

| NIU Shuhai , YANG Mengyao . Changes and policy adjustment suggestions of regional economic disparity in China[J]. Regional Economic Review, 2020, 2, 37- 43. | |

| 24 | KOENKER R . Quantile regression[M]. New York: Cambridge University Press, 2005. |

| 25 | HUBER P. The behavior of maximum likelihood estimates under nonstandard conditions[C]// Proceedings of the Fifth Berkeley Symposium on Mathematical Statistics and Probability, Berkeleg, USA: University of California Press, 1967, 1: 221-233. |

| 26 | HE Xuming , SHAO Qiman . A general Bahadur representation of M-estimators and its application to linear regression with nonstochastic designs[J]. The Annals of Statistics, 1996, 24 (6): 2608- 2630. |

| [1] | 任鹏程,徐静,李新民. 风险价值VaR的区间估计[J]. 山东大学学报(理学版), 2017, 52(2): 85-90. |

| [2] | 王小刚,李冰. 基于核函数方法的逐段线性Tobit回归模型估计[J]. 《山东大学学报(理学版)》, 2020, 55(6): 1-9. |

|