《山东大学学报(理学版)》 ›› 2023, Vol. 58 ›› Issue (11): 1-14,26.doi: 10.6040/j.issn.1671-9352.0.2022.265

• • 下一篇

杨鹏1( ),张晓燕2

),张晓燕2

Peng YANG1(),Xiaoyan ZHANG2

摘要:

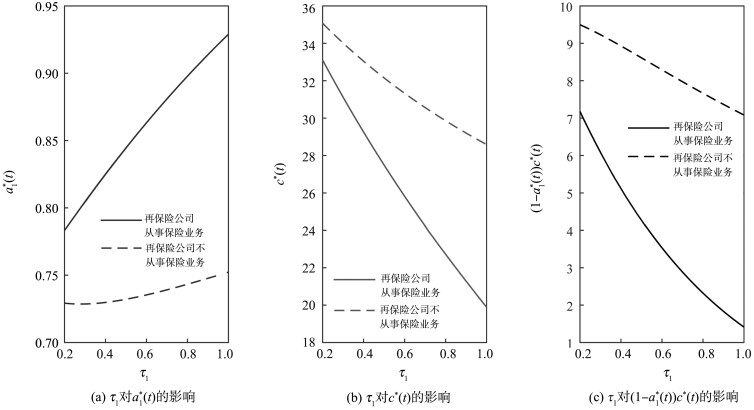

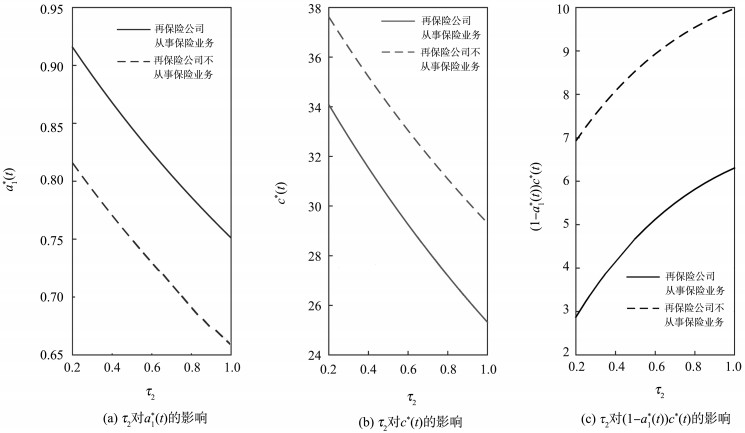

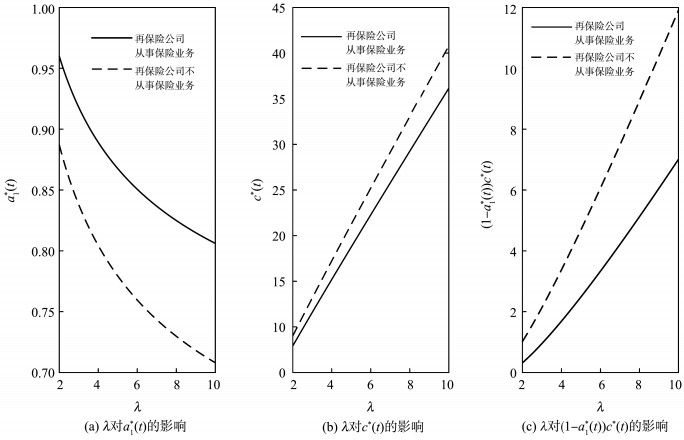

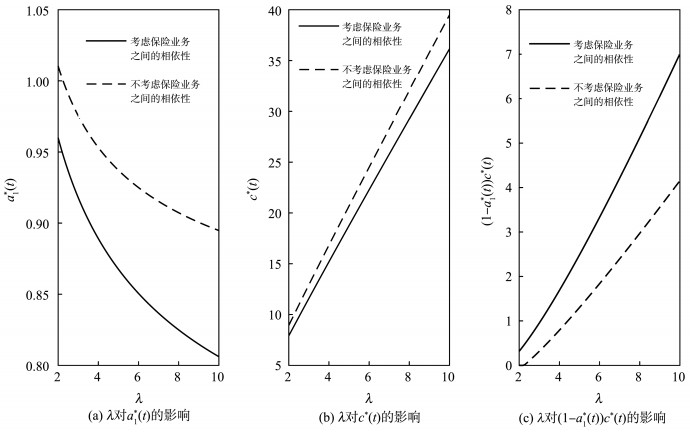

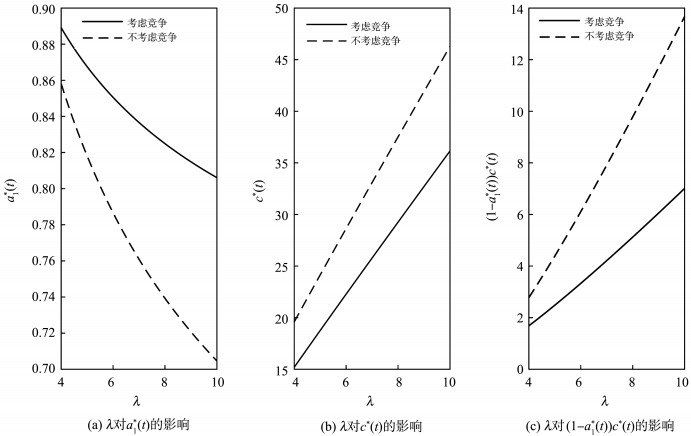

针对再保险合同设计问题, 即再保费的定价问题, 假设市场上有1家保险公司和1家再保险公司,其中, 保险公司从事2类保险业务, 再保险公司从事1类保险业务。为了体现保险公司与再保险公司之间的竞争, 假设3类保险业务具有相依性, 且允许保险公司从事再保险业务。利用相对业绩, 量化保险公司与再保险公司之间的竞争。保险公司和再保险公司的目标都是寻找最优的再保险合同, 最大化它们终端财富的均值同时最小化其方差。在Stackelberg博弈框架下, 通过使用随机分析和随机控制理论, 求得最优再保险合同和值函数的显式解。最终, 通过数值实验分析模型参数对最优再保险合同的影响, 比较一些特殊情形与一般情形的关系。

中图分类号:

| 1 |

RONG Ximin , YAN Yiqi , ZHAO Hui . Asymptotic solution of optimal reinsurance and investment problem with correlation risk for an insurer under the CEV model[J]. International Journal of Control, 2023, 96 (4): 840- 853.

doi: 10.1080/00207179.2021.2015627 |

| 2 |

ZHANG Yan , ZHAO Peibiao , TENG Xinghua , et al. Optimal reinsurance and investment strategies for an insurer and a reinsurer under Hestons SV model: HARA utility and Legendre transform[J]. Journal of Industrial and Management Optimization, 2021, 17 (4): 2139- 2159.

doi: 10.3934/jimo.2020062 |

| 3 |

CHEN Zhiping , YANG Peng . Robust optimal reinsurance-investment strategy with price jumps and correlated claims[J]. Insurance: Mathematics and Economics, 2020, 92, 27- 46.

doi: 10.1016/j.insmatheco.2020.03.001 |

| 4 |

LI Zhongfei , ZENG Yan , LAI Yongzeng . Optimal time-consistent investment and reinsurance strategies for insurers under Heston's SV models[J]. Insurance: Mathematics and Economics, 2012, 51 (1): 191- 203.

doi: 10.1016/j.insmatheco.2011.09.002 |

| 5 |

YANG Peng , CHEN Zhiping , WANG Liyuan . Time-consistent reinsurance and investment strategy combining quota-share and excess of loss for mean-variance insurers with jump-diffusion price process[J]. Communications in Statistics: Theory and Methods, 2021, 50 (11): 2546- 2568.

doi: 10.1080/03610926.2019.1670849 |

| 6 |

LIN Xiang , QIAN Yiping . Time-consistent mean-variance reinsurance-investment strategy for insurers under CEV model[J]. Scandinavian Actuarial Journal, 2016, 2016 (7): 646- 671.

doi: 10.1080/03461238.2015.1048710 |

| 7 |

YU Wenguang , GUO Peng , WANG Qi , et al. On a periodic capital injection and barrier dividend strategy in the compound Poisson risk model[J]. Mathematics, 2020, 8 (4): 511.

doi: 10.3390/math8040511 |

| 8 |

EISENBERG J , MISHURA Y . Optimising dividends and consumption under an exponential CIR as a discount factor[J]. Mathematical Methods of Operations Research, 2020, 92, 285- 309.

doi: 10.1007/s00186-020-00714-w |

| 9 |

HAN X , LIANG Z B , YOUNG V R . Optimal reinsurance to minimize the probability of drawdown under the mean-variance premium principle[J]. Scandinavian Actuarial Journal, 2020, 2020 (10): 879- 903.

doi: 10.1080/03461238.2020.1788136 |

| 10 | LUESAMAI A . Lower and upper bounds of the ultimate ruin probability in a discrete time risk model with proportional reinsurance and investment[J]. The Journal of Risk Management and Insurance, 2021, 25 (1): 1- 10. |

| 11 |

YUAN Yu , LIANG Zhibin , HAN Xia . Optimal investment and reinsurance to minimize the probability of drawdown with borrowing costs[J]. Journal of Industrial and Management Optimization, 2022, 18 (2): 933- 967.

doi: 10.3934/jimo.2021003 |

| 12 | PERCY D F , WARNER D B . Evaluating relative performances in disabled sports competitions[J]. IMA Journal of Management Mathematics, 2009, 20, 185- 199. |

| 13 |

DE MARZO P M , KANIEL R , KREMER I . Relative wealth concerns and financial bubbles[J]. The Review of Financial and Studies, 2008, 21 (1): 19- 50.

doi: 10.1093/rfs/hhm032 |

| 14 |

DENG Chao , ZENG Xudong , ZHU Huiming . Non-zero-sum stochastic differential reinsurance and investment games with default risk[J]. European Journal of Operational Research, 2018, 264 (3): 1144- 1158.

doi: 10.1016/j.ejor.2017.06.065 |

| 15 |

PUN C S , SIU C C , WONG H Y . Non-zero-sum reinsurance games subject to ambiguous correlations[J]. Operations Research Letters, 2016, 44 (5): 578- 586.

doi: 10.1016/j.orl.2016.06.004 |

| 16 |

HU Duni , WANG Hailong . Time-consistent investment and reinsurance under relative performance concerns[J]. Communications in Statistics: Theory and Methods, 2018, 47 (7): 1693- 1717.

doi: 10.1080/03610926.2017.1324987 |

| 17 |

CHEN Shumin , YANG Hailiang , ZENG Yan . Stochastic differential games between two insurers with generalized mean-variance premium principle[J]. ASTIN Bulletin, 2018, 48 (1): 413- 434.

doi: 10.1017/asb.2017.35 |

| 18 |

WANG Ning , ZHANG Nan , JIN Zhuo , et al. Stochastic differential investment and reinsurance games with nonlinear risk processes and VaR constraints[J]. Insurance: Mathematics and Economics, 2021, 96, 168- 184.

doi: 10.1016/j.insmatheco.2020.11.004 |

| 19 |

GU Ailing , CHEN Shumin , LI Zhongfei , et al. Optimal reinsurance pricing with ambiguity aversion and relative performance concerns in the principal-agent model[J]. Scandinavian Actuarial Journal, 2022, 2022 (9): 749- 774.

doi: 10.1080/03461238.2022.2026459 |

| 20 | YANG Peng , CHEN Zhiping . Optimal reinsurance pricing, risk sharing and investment strategies in a joint reinsurer-insurer framework[J]. IMA Journal of Management Mathematics, 2022, 34 (4): 661- 694. |

| 21 |

BÄUERLE N . Benchmark and mean-variance problems for insurers[J]. Mathematical Methods of Operations Research, 2005, 62 (1): 159- 165.

doi: 10.1007/s00186-005-0446-1 |

| 22 | BJÖRK T , MURGOCI A . A general theory of Markovian time inconsistent stochastic control problems[J]. SSRN Electronic Journal, 2010, 1, 55. |

| 23 |

YANG Peng , CHEN Zhiping , XU Ying . Time-consistent equilibrium reinsurance-investment strategy for n competitive insurers under a new interaction mechanism and a general investment framework[J]. Journal of Computational and Applied Mathematics, 2020, 374, 112769.

doi: 10.1016/j.cam.2020.112769 |

| [1] | 周驰,王艺馨,于静. 批发,代理还是混合?——与自营平台竞争的复合平台销售模式选择策略[J]. 《山东大学学报(理学版)》, 2023, 58(1): 89-100. |

| [2] | 肖敏,余敏,何新华. 引入垂直电商的供应链渠道定价策略[J]. 《山东大学学报(理学版)》, 2019, 54(3): 110-118. |

| [3] | 程茜,汪传旭,徐朗. 考虑利他偏好的低碳供应链决策[J]. 山东大学学报(理学版), 2018, 53(5): 41-52. |

| [4] | 张克勇1,吴燕1,侯世旺2. 零售商公平关切下闭环供应链定价策略研究[J]. J4, 2013, 48(05): 83-91. |

| [5] | 陆媛媛, . 基于渠道不对称的多品牌代理零售商的应对策略研究[J]. J4, 2008, 43(8): 19-23 . |

|