《山东大学学报(理学版)》 ›› 2024, Vol. 59 ›› Issue (1): 115-123.doi: 10.6040/j.issn.1671-9352.4.2022.205

徐圆圆1( ),郭红月1,*(),王利东2

),郭红月1,*(),王利东2

Yuanyuan XU1(),Hongyue GUO1,*(),Lidong WANG2

摘要:

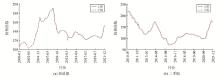

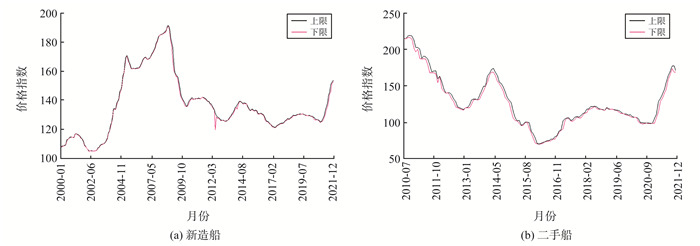

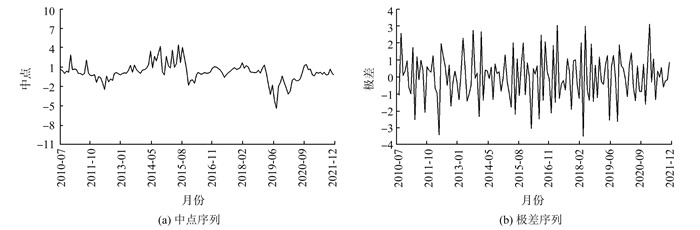

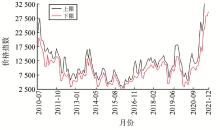

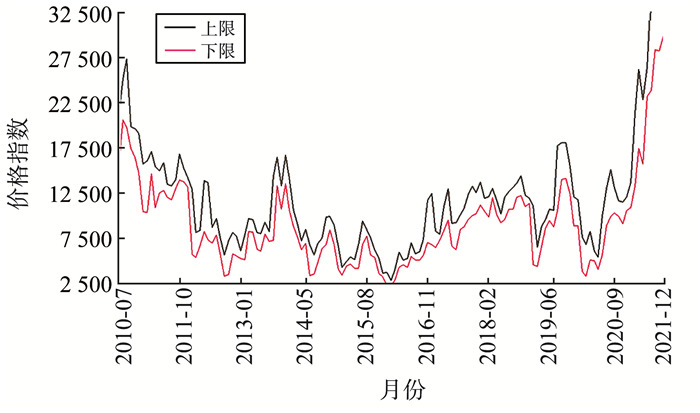

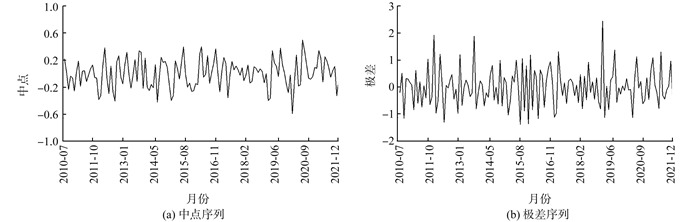

将远期运费协议(forward freight agreements, FFA)作为外生变量,研究其对船舶价格指数的具体影响。借助中点和极差方法, 分别建立区间型自回归模型和考虑区间型时间序列上、下限协整关系的区间型误差修正模型及带有外生变量FFA的区间型误差修正模型。将构建的模型用于对新造干散货船价格指数、二手干散货船价格指数进行的区间预测, 在平均绝对误差(MAE)、均方根误差(RMSE)指标上, 模型中加入协整项和FFA后预测精度更高。

中图分类号:

| 1 | 陈继红, 刘雯. 基于协整和VEC模型的VLCC新造船舶价格波动性[J]. 数学的实践与认识, 2016, 46 (24): 69- 78. |

| CHEN Jihong , LIU Wen . Fluctuation of the price of newbuilding VLCC ships based on cointegration and VEC model[J]. Mathematics in Practice and Theory, 2016, 46 (24): 69- 78. | |

| 2 | HER M T , CHUNG C C . Ship price predictions of panamax second-hand bulk carriers using grey models[J]. Journal of Marine Science and Technology, 2019, 27 (3): 229- 234. |

| 3 |

TGEODORE S , MICHAEL T . Support vector machine algorithms: an application to ship price forecasting[J]. Computational Economics, 2021, 57, 55- 87.

doi: 10.1007/s10614-020-10032-2 |

| 4 |

SYRIOPOULOS T , TSATSARONIS M , KARAMANOS I . Support vector machine algorithms: an application to ship price forecasting[J]. Computational Economics, 2021, 57, 55- 87.

doi: 10.1007/s10614-020-10032-2 |

| 5 |

GAO R , LIU J H , BAI X W , et al. Annual dilated convolution neural network for newbuilding ship prices forecasting[J]. Neural Computing and Applications, 2022, 34, 11853- 11863.

doi: 10.1007/s00521-022-07075-x |

| 6 |

GAO R B , LIU J H , DU L , et al. Shipping market forecasting by forecast combination mechanism[J]. Maritime Policy and Management, 2022, 49 (8): 1059- 1074.

doi: 10.1080/03088839.2021.1945698 |

| 7 |

WANG X , ZHANG Z , LI S . Set-valued and interval-valued stationary time series[J]. Journal of Multivariate Analysis, 2016, 145, 208- 223.

doi: 10.1016/j.jmva.2015.12.010 |

| 8 |

SUN Y Y , HAN A , HONG Y M , et al. Threshold autoregressive models for interval valued time series data[J]. Journal of Econometrics, 2018, 206 (2): 414- 446.

doi: 10.1016/j.jeconom.2018.06.009 |

| 9 | MOORE R E. Interval analysis[D]. Englewood Cliffs: Prentice-Hall, 1966. |

| 10 | LIMA N , DE CARVALHO F A . An exponential-type kernel robust regression model for interval-valued variables[J]. Information Sciences, 2018, 2018 (454/455): 419- 442. |

| 11 | BILLARD L, DIDAY E. Regression analysis for interval-valued data & data analysis, classification and related methods[C]//Proceedings of the Seventh Conference of the International Federation of Classification Societies. Belgium: Springer, 2000: 369-374. |

| 12 |

BILLARD L , DIDAY E . From the statistics of data to the statistics of knowledge: symbolic data analysis[J]. Journal of the American Statistical Association, 2003, 98 (462): 470- 487.

doi: 10.1198/016214503000242 |

| 13 |

NETO L E A , CARVALHO F A T . Center and range method for fitting a linear regression model to symbolic interval data[J]. Computational Statistics and Data Analysis, 2008, 52 (3): 1500- 1515.

doi: 10.1016/j.csda.2007.04.014 |

| 14 |

NETO L E A , CARVALHO F A T . Constrained linear regression models for symbolic interval-valued variables[J]. Computational Statistics and Data Analysis, 2010, 54 (2): 333- 347.

doi: 10.1016/j.csda.2009.08.010 |

| 15 | HAN A , HONG Y M , WANG S Y , et al. A vector autoregressive moving average model for interval-valued time series data[J]. Advances in Econometrics, 2016, 36, 417- 460. |

| 16 |

YANG W , HAN A , WANG S Y . Analysis of crisis impact on crude oil prices: a new approach with interval time series modelling[J]. Quantitative Finance, 2016, 16 (12): 1917- 1928.

doi: 10.1080/14697688.2016.1211795 |

| 17 | 杨威, 韩艾, 汪寿阳. 基于区间型数据的金融时间序列预测研究[J]. 系统工程学报, 2016, 31 (6): 817- 831. |

| YANG Wei , HAN Ai , WANG Shouyang . Research on financial time Series prediction based on interval data[J]. Journal of Systems Engineering, 2016, 31 (6): 817- 831. | |

| 18 | 陈炜, 徐慧琳, 汪寿阳, 等. 基于误差修正与分解的区间值股价时间序列预测研究[J]. 系统工程理论与实践, 2023, 43 (2): 383- 397. |

| CHEN Wei , XU Huilin , WANG Shouyang , et al. Error correction and decomposition method for forecast of interval-valued stock price time series[J]. Systems Engineering-Theory and Practice, 2023, 43 (2): 383- 397. | |

| 19 | 闵德权, 张鑫, 崔琪. 远期运费协议与新造船市场的波动溢出效应研究[J]. 中国水运, 2019, 19 (12): 37- 39. |

| MIN Dequan , ZHANG Xin , CUI Qi . A study on volatility spillover effects of forward freight agreements and new shipbuilding market[J]. China Water Transport, 2019, 19 (12): 37- 39. | |

| 20 |

杨芊, 林国龙, 丁一. FFA市场与二手船市场的波动溢出效应[J]. 武汉理工大学学报(交通科学与工程版), 2015, 39 (5): 1001- 1004.

doi: 10.3963/j.issn.2095-3844.2015.05.022 |

|

YANG Qian , LIN Guolong , DING Yi . Volatility spillover effects between forward freight market and second-hand ship maket[J]. Journal of Wuhan University of Technology (Transportation Science and Engineering), 2015, 39 (5): 1001- 1004.

doi: 10.3963/j.issn.2095-3844.2015.05.022 |

|

| 21 | 陶志富, 刘金培, 朱家明, 等. 区间值时间序列预测效果测度研究[J]. 模糊系统与数学, 2018, 32 (4): 135- 144. |

| TAO Zhifu , LIU Jinpei , ZHU Jiaming , et al. Study on measurement of interval-value time series prediction effect[J]. Fuzzy Systems and Mathematics, 2018, 32 (4): 135- 144. |

| No related articles found! |

|