《山东大学学报(理学版)》 ›› 2019, Vol. 54 ›› Issue (5): 77-87.doi: 10.6040/j.issn.1671-9352.0.2018.453

邹绍辉1,2( ),张甜3,*(),闫晓霞1,2

),张甜3,*(),闫晓霞1,2

Shao-hui ZOU1,2(),Tian ZHANG3,*(),Xiao-xia YAN1,2

摘要:

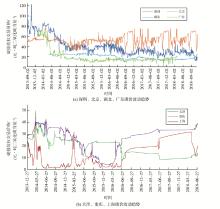

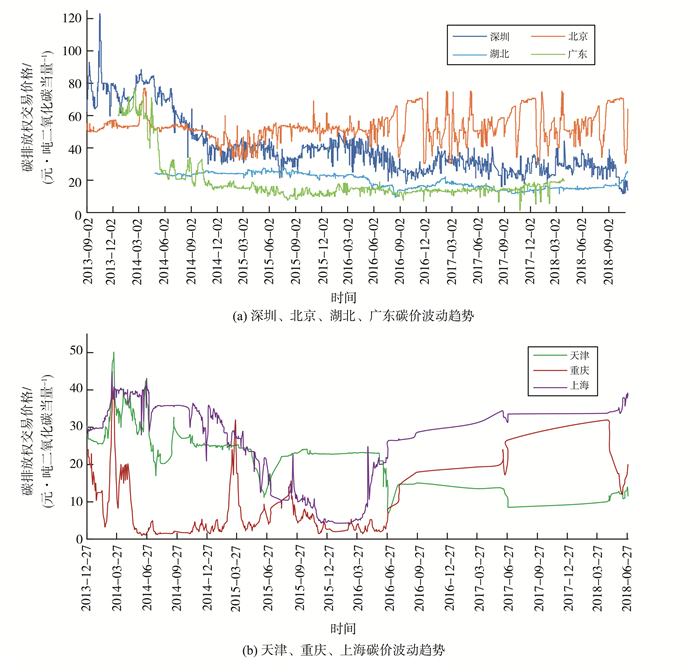

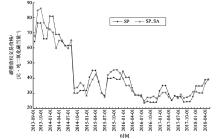

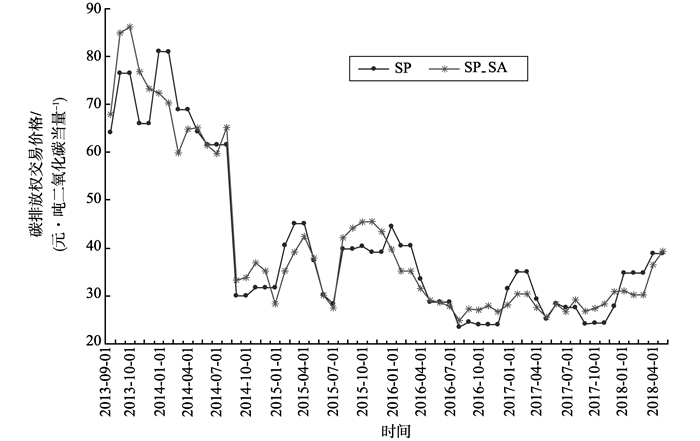

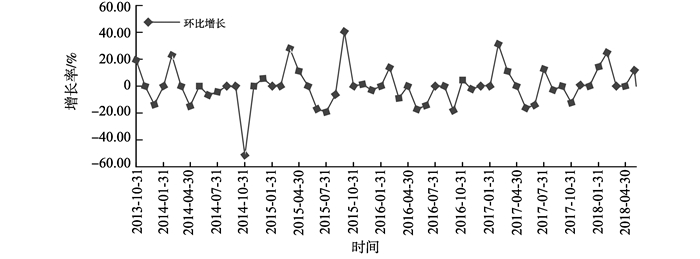

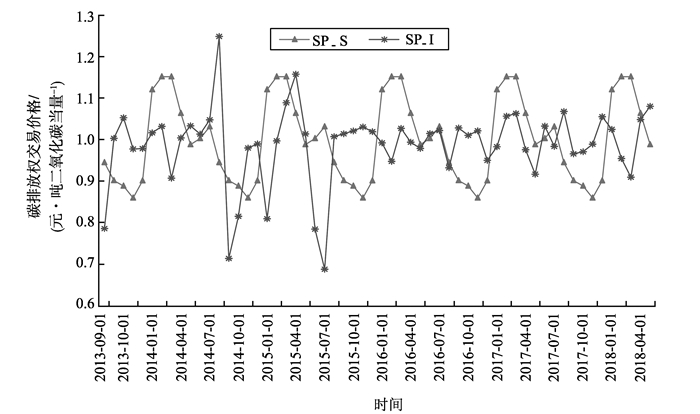

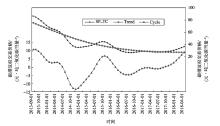

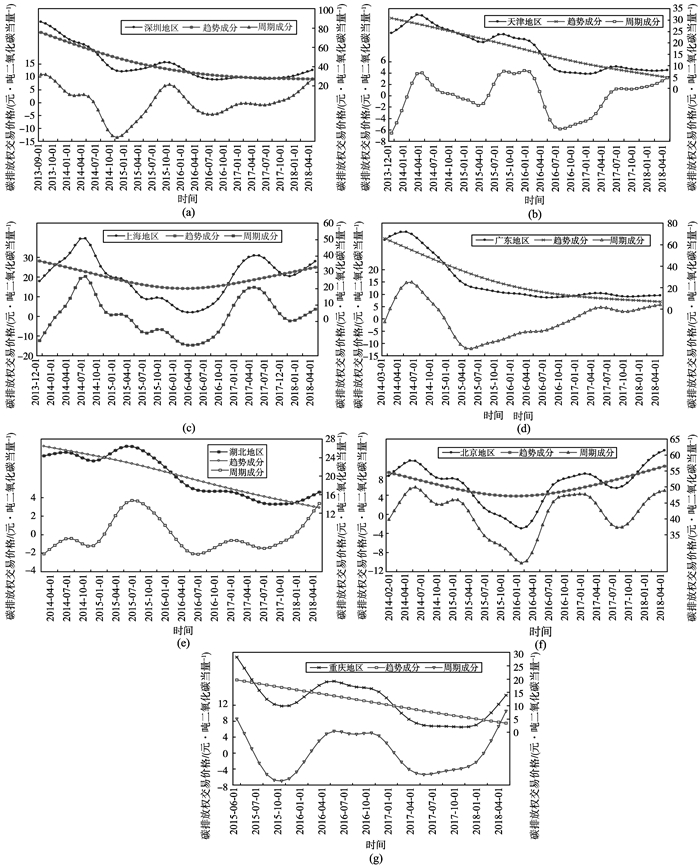

我国碳排放权交易价格具有明显的波动性和地区差异性,科学刻画碳排放权交易价格的波动性和解析不同地区的差异性有利于规避投资风险、平稳发展碳市场和提高国内碳市场在国际市场的定价能力,对加快建立全国统一碳市场也尤为重要。H-P滤波法是经常使用的经济变量趋势分解方法,可有效地解析时间序列数据中的季节变动规律。选取2013年12月至2018年6月之间国内7大区碳市场域碳排放权交易价格月度数据,采用H-P滤波法实证研究了国内碳价波动规律和区域特征。研究结果表明,国内碳价具备“波动中下降”的显著特征,呈现3个完整周期,每个周期时间范围在10~22个月之间,峰值与谷值都呈现不同程度的下降趋势且均由正变负,周期类型都表现出陡降趋势;从区域影响看,天津和北京的碳排放权交易价格的波动一致特征更明显,而湖北和重庆的碳排放权交易价格波动对天津的影响程度较小。

中图分类号:

| 1 |

周天芸, 许锐翔. 中国碳排放权交易价格的形成及其波动特征—基于深圳碳排放权交易所的数据[J]. 金融发展研究, 2016, (1): 16- 25.

doi: 10.3969/j.issn.1674-2265.2016.01.003 |

|

ZHOU Tianyun , XU Ruixiang . The formation and volitility features of China's carbon emission trading price: based on the data of Shenzhen carbon emission exchange[J]. Journal of Financial Development Research, 2016, (1): 16- 25.

doi: 10.3969/j.issn.1674-2265.2016.01.003 |

|

| 2 | 吕勇斌, 邵律博. 我国碳排放权价格波动特征研究:基于GARCH族模型的分析[J]. 价格理论与实践, 2015, (12): 62- 64. |

| LYU Yongbin , SHAO Lyubo . Study on the price fluctuation characteristics of carbon emission rights in China based on GARCH family model[J]. Price:Theory & Practice, 2015, (12): 62- 64. | |

| 3 | ZHANG Y. Pricing decision theory and the empirical research on international carbon emissions trading[C]//International Conference on Computer Science and Electronics Engineering. Hangzhou: IEEE, 2012: 6-10. |

| 4 |

JOYEUX R , MILUNOVICH G . Testing market efficiency in the EU carbon futures market[J]. Applied Financial Economics, 2010, 20 (10): 803- 809.

doi: 10.1080/09603101003636220 |

| 5 |

FANG G C , TIAN L X , LIU M H , et al. How to optimize the development of carbon trading in China: enlightenment from evolution rules of the EU carbon price[J]. Applied Energy, 2018, 211: 1039- 1049.

doi: 10.1016/j.apenergy.2017.12.001 |

| 6 |

ZHAO X G , JIANG G W , NIE D , et al. How to improve the market efficiency of carbon trading: a perspective of China[J]. Renewable and Sustainable Energy Reviews, 2016, 59: 1229- 1245.

doi: 10.1016/j.rser.2016.01.052 |

| 7 |

ZHAO X G , WU L , LI A . Research on the efficiency of carbon trading market in China[J]. Renewable and Sustainable Energy Reviews, 2017, 79: 1- 8.

doi: 10.1016/j.rser.2017.05.034 |

| 8 |

CONG R , LO A Y . Emission trading and carbon market performance in Shenzhen, China[J]. Applied Energy, 2017, 193: 414- 425.

doi: 10.1016/j.apenergy.2017.02.037 |

| 9 | 袁嫄, 刘纪显, 张芳. 碳配额市场价格非对称性波动研究:基于欧盟碳配额管理制度的实证分析[J]. 金融论坛, 2015, 20 (5): 44- 53, 70. |

| YUAN Yuan , LIU Jixian , ZHANG Fang . A study of the asymmetry fuctuation in the price of carbon quota market: an analysis based on the management system of EU carbon quota[J]. Finance Forum, 2015, 20 (5): 44- 53, 70. | |

| 10 | 胡根华, 吴恒煜. 资产价格的时变跳跃:碳排放交易市场的证据[J]. 中国人口资源与环境, 2015, 25 (11): 12- 18. |

| HU Genhua , WU Hengyu . Time-varying jumps of capital's price: evidence from carbon emission trading market[J]. China Population, Resources and Environment, 2015, 25 (11): 12- 18. | |

| 11 | 刘承智, 潘爱玲, 谢涤宇. 我国碳排放权交易市场价格波动问题探讨[J]. 价格理论与实践, 2014, (8): 55- 57. |

| LIU Chengzhi , PAN Ailing , XIE Diyu . Price fluctuation in China's carbon emission trading market[J]. Price:Theory & Practice, 2014, (8): 55- 57. | |

| 12 | 汪文隽, 周婉云, 李瑾, 等. 中国碳市场波动溢出效应研究[J]. 中国人口·资源与环境, 2016, 26 (12): 63- 69. |

| WANG Wenjun , ZHOU Wanyun , LI Jin , et al. Volatility spillovers among Chinese carbon markets[J]. China Population, Resources and Environment, 2016, 26 (12): 63- 69. | |

| 13 |

张晨, 杨仙子. 基于多频组合模型的中国区域碳市场价格预测[J]. 系统工程理论与实践, 2016, 36 (12): 3017- 3025.

doi: 10.12011/1000-6788(2016)12-3017-09 |

|

ZHANG Chen , YANG Xianzi . Forecasting of China's regional carbon market price based on multi-frequency combined model[J]. Systems Engineering-Theory & Practice, 2016, 36 (12): 3017- 3025.

doi: 10.12011/1000-6788(2016)12-3017-09 |

|

| 14 | 邹绍辉, 张甜. 国际碳期货价格与国内碳价动态关系[J]. 山东大学学报(理学版), 2018, 53 (5): 70- 79. |

| ZOU Shaohui , ZHANG Tian . Interaction relationship between international carbon future price and domestic carbon price[J]. Journal of Shandong University (Natural Science), 2018, 53 (5): 70- 79. | |

| 15 | 郭白滢, 周任远. 我国碳交易市场价格周期及其波动性特征分析[J]. 统计与决策, 2016, (21): 154- 157. |

| GUO Baihao , ZHOU Renyuan . Analysis of price cycle and volatility characteristics of China's carbon trading market[J]. Statistics & Decision, 2016, (21): 154- 157. | |

| 16 | 白云帆.欧盟碳排放权市场价格波动规律研究[D].广州:暨南大学, 2016. |

| BAI Yunfan. The study on the price fluctuation laws of EU ETS[D]. Guangzhou: Jinan University, 2016. | |

| 17 | HODRICK R, PRESCOTT E. Postwar U.S. business cycles[M]//Real Business Cycles. London: Routledge, 1998: 593-608. |

| [1] | 邹绍辉,张甜. 国际碳期货价格与国内碳价动态关系[J]. 山东大学学报(理学版), 2018, 53(5): 70-79. |

| [2] | 董振宁,王卓,周雪君. 限制贷款最低额度的零售商融资与订货决策[J]. 山东大学学报(理学版), 2018, 53(5): 61-69. |

| [3] | 陈丽,林玲. 具有时滞效应的股票期权定价[J]. 山东大学学报(理学版), 2018, 53(4): 36-41. |

| [4] | 刘昆仑. 变结构pair copula模型在金融危机传染分析中的应用[J]. 山东大学学报(理学版), 2016, 51(6): 104-110. |

| [5] | 赵攀, 肖庆宪. 基于Tsalli熵分布及O-U过程的幂式期权定价[J]. 山东大学学报(理学版), 2015, 50(04): 1-7. |

| [6] | 孙 鹏,赵卫东 . 亚式期权定价问题的交替方向迎风有限体积方法[J]. J4, 2007, 42(6): 16-21 . |

| [7] | 马玉林,王希泉 . 基于实际波动率的VaR模型实证研究[J]. J4, 2007, 42(10): 84-89 . |

| [8] | 杨维强,彭实戈 . 期权稳健定价模型及实证[J]. J4, 2006, 41(2): 69-73 . |

| [9] | 安起光,王厚杰 . 基于机会约束的均值—VaR投资组合模型再研究[J]. J4, 2006, 41(2): 94-100 . |

| [10] | 史开泉 . 函数S-粗集与投资风险F-规律发现[J]. J4, 2007, 42(1): 1-7 . |

|