《山东大学学报(理学版)》 ›› 2024, Vol. 59 ›› Issue (8): 94-102.doi: 10.6040/j.issn.1671-9352.0.2023.206

屈忠锋( ),吴鸿华,李凡军

),吴鸿华,李凡军

Zhongfeng QU(),Honghua WU,Fanjun LI

摘要:

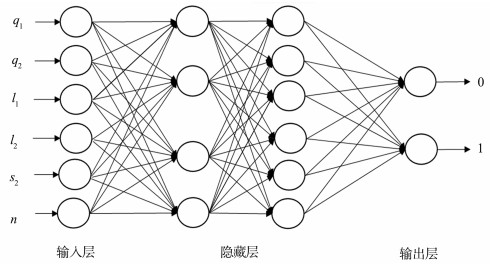

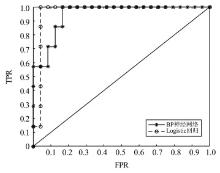

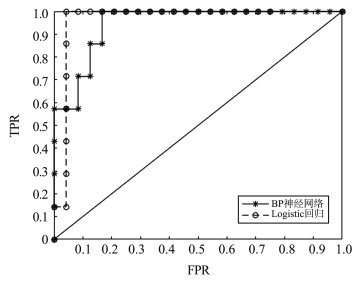

为了便于银行对中小企业进行信贷风险评估,同时制定最优信贷策略,利用企业与上下游合作伙伴的银行流水信息,构建企业营业收入能力、盈利能力、客户稳定性、交易活力4个一级指标组成的风险评估指标体系;基于Logistic回归对企业信贷风险进行预测,并与误差反向传播神经网络进行了对比分析;结合违约概率与不同利率下的留存率,以银行对中小企业的最大化期望收益为目标函数,建立信贷策略优化模型;对信贷风险评估和信贷策略优化模型分别进行实证分析,验证模型的有效性。结果表明:Logistic回归具有较高的准确率和查全率,评估指标受试者工作特征曲线下面积达到0.964,适合中小企业的信贷风险预测和评估;所建立的信贷策略优化模型能确定每个贷款企业的贷款额度和贷款利率,并使银行期望收益达到最大。

中图分类号:

| 1 | 中国人民银行. 人民银行、银保监会"小微企业金融服务有关情况"新闻发布会文字实录[EB/OL]. (2019-06-25)[2024-04-22]. http://www.gov.cn/xinwen/2019-06/26/content_544116.htm. |

| 2 |

ALTMAN E I . Financial ratios, discriminant analysis and the prediction of corporate bankruptcy[J]. The Journal of Finance, 1968, 23 (4): 589- 609.

doi: 10.1111/j.1540-6261.1968.tb00843.x |

| 3 | ALTMAN E I , HALDEMAN R G , NARAYANAN P . ZETATM analysis: a new model to identify bankruptcy risk of corporations[J]. Journal of Banking & Finance, 1977, 1 (1): 29- 54. |

| 4 | MERTON R C . On the pricing of corporate debt: the risk structure of interest rates[J]. The Journal of Finance, 1974, 29 (2): 449- 470. |

| 5 |

MIN J H , LEE Y C . Bankruptcy prediction using support vector machine with optimal choice of kernel function parameters[J]. Expert Systems with Applications, 2005, 28 (4): 603- 614.

doi: 10.1016/j.eswa.2004.12.008 |

| 6 |

KUKUK M , RÖNNBERG M . Corporate credit default models: a mixed logit approach[J]. Review of Quantitative Finance and Accounting, 2013, 40 (3): 467- 483.

doi: 10.1007/s11156-012-0281-4 |

| 7 |

ABID L , MASMOUDI A , ZOUARI-GHORBEL S . The consumer loan's payment default predictive model: an application of the Logistic regression and the discriminant analysis in a Tunisian commercial bank[J]. Journal of the Knowledge Economy, 2018, 9 (3): 948- 962.

doi: 10.1007/s13132-016-0382-8 |

| 8 | 吴世农, 卢贤义. 我国上市公司财务困境的预测模型研究[J]. 经济研究, 2001, (6): 46- 55. |

| WU Shinong , LU Xianyi . A study of models for predicting financial distress in China's listed companies[J]. Economic Research Journal, 2001, (6): 46- 51. | |

| 9 |

糜仲春, 申义, 张学农. 我国商业银行中小企业信贷风险评估体系的构建[J]. 金融论坛, 2007, (3): 21- 25.

doi: 10.3969/j.issn.1009-9190.2007.03.004 |

|

MI Zhongchun , SHEN Yi , ZHANG Xuenong . Establishing a credit risk evaluation system for SMZ enterprises by our commer cial banks[J]. Finance Forum, 2007, (3): 21- 25.

doi: 10.3969/j.issn.1009-9190.2007.03.004 |

|

| 10 | 郭妍, 张立光, 刘佳. 中小企业信贷风险度量模型研究: 基于山东省的实证分析[J]. 东岳论丛, 2013, 34 (7): 58- 61. |

| GUO Yan , ZHANG Liguang , LIU Jia . Research on the credit risk measurement model for small and medium enterprises: an empirical analysis based on Shandong Province[J]. Dongyue Tribune, 2013, 34 (7): 58- 61. | |

| 11 | 张雷. 基于混合遗传算法-支持向量机的中小型企业信用评估模型[J]. 河南师范大学学报(自然科学版), 2022, 50 (2): 79- 85. |

| ZHANG Lei . Credit evaluation on model of small and mediun-sized enterprices based on HGA-SVM[J]. Journal of Henan Normal University (Natural Science Edition), 2022, 50 (2): 79- 85. | |

| 12 |

程扬, 周大勇, 程帆, 等. 基于组合赋权法的中小微企业信贷风险量化及预测[J]. 系统工程, 2023, 41 (1): 140- 151.

doi: 10.3969/j.issn.1001-2362.2023.01.046 |

|

CHENG Yang , ZHOU Dayong , CHENG Fan , et al. Quantification forecast of credit risk of small and medium-sized enterprises based on combination weighting method[J]. Systems Engineering, 2023, 41 (1): 140- 151.

doi: 10.3969/j.issn.1001-2362.2023.01.046 |

|

| 13 |

钱慧, 梅强, 文学舟. 小微企业信贷风险评估实证研究[J]. 科技管理研究, 2013, 33 (14): 220- 223.

doi: 10.3969/j.issn.1000-7695.2013.14.050 |

|

QIAN Hui , MEI Qiang , WEN Xuezhou . Research of small and micro enterprises' credit risk evaluation[J]. Science and Technology Management Research, 2013, 33 (14): 220- 223.

doi: 10.3969/j.issn.1000-7695.2013.14.050 |

|

| 14 |

严社燕, 刘菁, 马飞杨, 等. 基于因子分析和BP神经网络的中小微企业信誉等级研究[J]. 商展经济, 2022, (15): 147- 149.

doi: 10.12245/j.issn.2096-6776.2022.15.3217 |

|

YAN Sheyan , LIU Jing , MA Feiyang , et al. Research on credit rating of small and medium sized enterprises based on factor analysis and BP neural network[J]. Trade Fair Economy, 2022, (15): 147- 149.

doi: 10.12245/j.issn.2096-6776.2022.15.3217 |

|

| 15 | 王志勇, 杨旭, 吴嘉津. 中小微企业信贷策略研究[J]. 数学建模及其应用, 2021, 10 (1): 80- 91. |

| WANG Zhiyong , YANG Xu , WU Jiajin . The study on crecit strategy for MSMEs[J]. Mathematical Modeling and Its Applications, 2021, 10 (1): 80- 91. | |

| 16 |

郁蓥荧, 鲍琴, 戴柯磊. 基于风险与收益平衡的银行信贷策略模型构建及可行性分析[J]. 经济研究导刊, 2022, (13): 95- 98.

doi: 10.3969/j.issn.1673-291X.2022.13.029 |

|

YU Yingying , BAO Qin , DAI Kelei . Construction and feasibility analysis of a bank credit strategy model based on risk and return balance[J]. Conomic Research Guided, 2022, (13): 95- 98.

doi: 10.3969/j.issn.1673-291X.2022.13.029 |

|

| 17 | 吕秀梅. 大数据金融下的中小微企业信用评估[J]. 财会月刊, 2019, (13): 22- 27. |

| LÜ Xiumei . Credit evaluation of small and medium-sized enterprises under big data finance[J]. Finance and Accounting Monthly, 2019, (13): 22- 27. | |

| 18 | 胡兆钧. 小微企业客户违约与交易流水之间关系的实证研究[D]. 上海: 上海交通大学, 2017. |

| HU Zhaojun. A study on the relationship between the small-sized enterprises' default and the transaction flow[D]. Shanghai: Shanghai Jiaotong University, 2017. | |

| 19 | 王跃. 上市民营企业信贷风险识别的双模型预测方法比较研究[D]. 包头: 内蒙古科技大学, 2020. |

| WANG Yue. A comparative study on the credit risk identification of private listed companies with dual model prediction method[D]. Baotou: Inner Mongolia University of Science & Technology, 2020. | |

| 20 | 白羽, 三郎斯基, 王晓妍, 等. 基于层次分析法量化中小微企业信贷风险[J]. 北京建筑大学学报, 2021, 37 (2): 93- 97. |

| BAI Yu , SANLANG Siji , WANG Xiaoyan , et al. Quantification of the credit risk of medium, small and micro-sized enterprises based on analytic hierarchy process[J]. Journal of Beijing University of Civil Engineering and Architecture, 2021, 37 (2): 93- 97. | |

| 21 |

朱强军. 基于改进的TOPSIS算法的企业信贷风险评价: 以中小微企业为例[J]. 长春大学学报, 2022, 32 (7): 24- 33.

doi: 10.3969/j.issn.1009-3907.2022.07.004 |

|

ZHU Qiangjun . Evaluation of enterprise credit loan risk based on the improved TOPSIS algorithm: taking small and medium-sized enterprises as an example[J]. Journal of Changchun University, 2022, 32 (7): 24- 33.

doi: 10.3969/j.issn.1009-3907.2022.07.004 |

| [1] | 张要,马盈仓,杨小飞,朱恒东,杨婷. 结合流形结构与柔性嵌入的多标签特征选择[J]. 《山东大学学报(理学版)》, 2021, 56(7): 91-102. |

|