《山东大学学报(理学版)》 ›› 2024, Vol. 59 ›› Issue (4): 98-107.doi: 10.6040/j.issn.1671-9352.0.2022.629

张亚茹1( ),夏莉1,2,*(),张典秋1

),夏莉1,2,*(),张典秋1

Yaru ZHANG1(),Li XIA1,2,*(),Dianqiu ZHANG1

摘要:

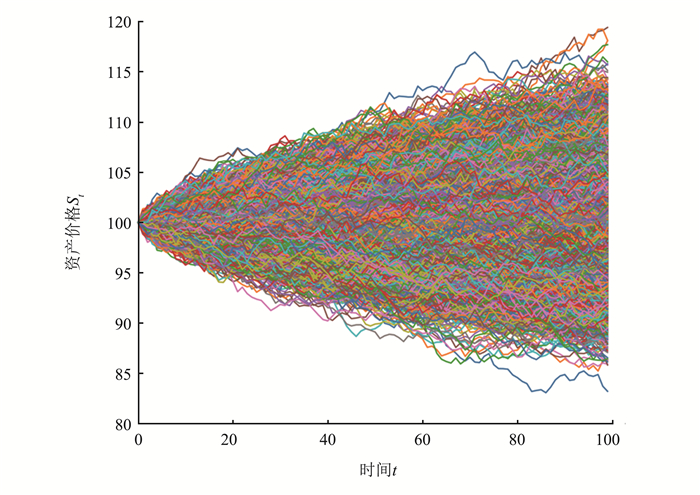

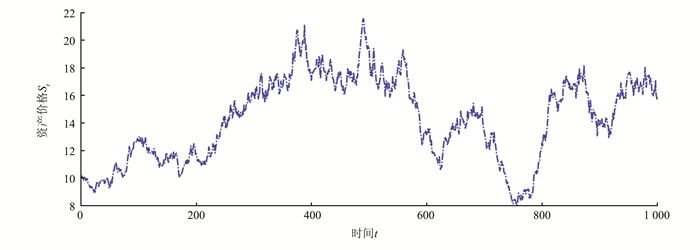

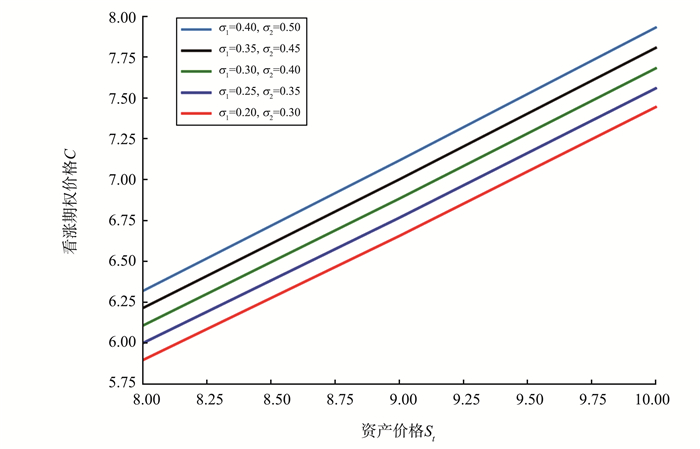

构建混合双分数布朗运动驱动下的带有红利的永久美式回望期权定价模型。首先,通过Δ-对冲原理,给出混合双分数布朗运动下的永久美式回望看涨和看跌期权所满足的偏微分方程组;其次,通过变量代换法、特征方程法对建立的偏微分方程组进行求解,给出混合双分数布朗运动下的永久美式回望看涨和看跌期权定价公式及其最佳实施边界;最后,通过数值实验,验证该解的线性等比例缩放性质,并讨论混合双分数布朗运动参数H、K及波动率对期权价格的影响。

中图分类号:

| 1 | SHREVES E.Stochastic calculus for finance Ⅱ: continuous-time models[M].New York:Springer,2004. |

| 2 | GOLDMANM B,SOSINH B,GATTOM A.Path dependentoptions: "buy at the low, sell at the high"[J].The Journal of Finance,1979,34(5):1111-1127. |

| 3 |

EMANUELD C,MACBETHJ D.Further results on the constant elasticity of variance call option pricing model[J].Journal of Financial and Quantitative Analysis,1982,17(4):533-554.

doi: 10.2307/2330906 |

| 4 |

DAIMin.A closed-form solution for perpetual American floating strike lookback options[J].Journal of Computational Finance,2000,4(2):63-68.

doi: 10.21314/JCF.2001.074 |

| 5 | 姜礼尚.期权定价的数学模型和方法[M].2版北京:高等教育出版社,2008. |

| JIANGLishang.Mathematical modeling and methods of option pricing[M].2nd edBeijing:Higher Education Press,2008. | |

| 6 |

张艳秋,杜雪樵.随机利率下的回望期权的定价[J].合肥工业大学学报(自然科学版),2007,30(4):515-517.

doi: 10.3969/j.issn.1003-5060.2007.04.031 |

|

ZHANGYanqiu,DUXueqiao.Pricing of lookback options under stochastic interest rates[J].Journal of Hefei University of Technology (Natural Science),2007,30(4):515-517.

doi: 10.3969/j.issn.1003-5060.2007.04.031 |

|

| 7 | 袁国军,肖庆宪.CEV过程下有交易费的回望期权定价研究[J].系统工程学报,2011,26(5):642-648. |

| YUANGuojun,XIAOQingxian.Study of pricing lookback options in CEV process with transaction cost[J].Journal of Systems Engineering,2011,26(5):642-648. | |

| 8 |

TINGS H M,EWALDC O,WANGW K.On the investment-uncertainty relationship in a real option model with stochastic volatility[J].Mathematical Social Sciences,2013,66(1):22-32.

doi: 10.1016/j.mathsocsci.2013.01.005 |

| 9 | 桑利恒.标的资产带有红利支付的回望期权定价[J].长春大学学报,2014,24(12):1671-1674. |

| SANGLiheng.Valuation of lookback option of underlying asset with dividend payment[J].Journal of Changchun University,2014,24(12):1671-1674. | |

| 10 | 陈海珍,周圣武,孙祥艳.混合分数布朗运动下的回望期权定价[J].华东师范大学学报(自然科学版),2018,(4):47-58. |

| CHENHaizhen,ZHOUShengwu,SUNXiangyan.Pricing of lookback options under a mixed fractional Brownian movement[J].Journal of East China Normal University (Natural Science),2018,(4):47-58. | |

| 11 | DENGGuohe.Pricing perpetual American floating strike lookback option under multiscale stochastic volatility model[J].Chaos, Solitons & Fractals,2020,141,110411. |

| 12 | 顾哲煜. 几类混合双分数布朗运动模型下回望期权的定价研究[D]. 南京: 南京财经大学, 2020. |

| GU Zheyu. Research on the pricing of lookback options under several mixed bi-fractional Brownian motion models[D]. Nanjing: Nanjing University of Finance and Economics, 2020. | |

| 13 | 安翔,郭精军.混合次分数布朗运动下永久美式回望期权的定价[J].应用数学,2021,34(4):820-828. |

| ANXiang,GUOJingjun.Pricing of perpetual American lookback option under the sub-mixed fractional Brownian motion[J].Mathematica Applicate,2021,34(4):820-828. | |

| 14 | 安翔,郭精军.混合次分数跳扩散模型下回望期权的定价及模拟[J].山东大学学报(理学版),2022,57(4):100-110. |

| ANXiang,GUOJingjun.Pricing and simulation of lookback options under the mixed sub-fractional jump-diffusion model[J].Journal of Shandong University (Natural Science),2022,57(4):100-110. | |

| 15 | 张萌,温鲜,霍海峰.基于次分数布朗运动的欧式回望期权定价[J].桂林航天工业学院学报,2022,27(1):110-115. |

| ZHANGMeng,WENXian,HUOHaifeng.European lookback option pricing based on fractional Brownian motion[J].Journal of Guilin University of Aerospace Technology,2022,27(1):110-115. | |

| 16 | 杨朝强,田有功.一类杠杆公司的破产概率: 回望期权定价方法[J].应用概率统计,2022,38(1):1-23. |

| YANGZhaoqiang,TIANYougong.Bankruptcy probability of a lever company: lookback option pricing method[J].Chinese Journal of Applied Probability and Statistics,2022,38(1):1-23. | |

| 17 | ZHANGXili,XIAOWeilin.Arbitrage with fractional Gaussian processes[J].Physica A: Statistical Mechanics and its Applications,2017,471,620-628. |

| 18 | RUSSOF,TUDORC A.On bifractional Brownian motion[J].Stochastic Processes and their Applications,2006,116(5):830-856. |

| [1] | 彭波,郭精军. 在跳环境和混合高斯过程下的资产定价及模拟[J]. 《山东大学学报(理学版)》, 2020, 55(5): 105-113. |

| [2] | 陈丽,林玲. 具有时滞效应的股票期权定价[J]. 山东大学学报(理学版), 2018, 53(4): 36-41. |

| [3] | 李国成,王继霞. 交叉熵蝙蝠算法求解期权定价模型参数估计问题[J]. 《山东大学学报(理学版)》, 2018, 53(12): 80-89. |

| [4] | 郭尊光1,孔涛2*,李鹏飞2, 张微2. 基于最优实施边界的美式期权定价的数值方法[J]. J4, 2012, 47(3): 110-119. |

| [5] | 张慧1,2,孟纹羽1,来翔3. 不确定环境下障碍再装期权的动态定价模型 ——基于BSDE解的期权定价方法[J]. J4, 2011, 46(3): 52-57. |

| [6] | 陈祥利. 脆弱期权的公司价值分形定价模型[J]. J4, 2010, 45(11): 109-114. |

| [7] | 孙 鹏,张 蕾,赵卫东 . 美式期权定价问题的一类有限体积数值模拟方法[J]. J4, 2007, 42(6): 1-06 . |

| [8] | 孙 鹏,赵卫东 . 亚式期权定价问题的交替方向迎风有限体积方法[J]. J4, 2007, 42(6): 16-21 . |

| Viewed | ||||||||||||||||||||||||||||||||||||||||||||||||||

|

Full text 452

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||

|

Abstract 408

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||

Cited |

|

|||||||||||||||||||||||||||||||||||||||||||||||||

| Shared | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Discussed | ||||||||||||||||||||||||||||||||||||||||||||||||||

|